BERITA TERKINI

JAKARTA, DDTCNews - The Directorate General of Taxes (DJP) is once again reminding taxpayers to understand the provisions regarding the debt-to-equity ratio (DER). It is important to note that a company's debt is not merely a financial matter — it can also affect the amount of corporate income tax owed.

Through the DER provisions, the government regulates the acceptable limit between a company's debt and equity to prevent tax avoidance through excessive interest expenses. So what constitutes a healthy DER? What are the consequences if a company's debt ratio is too high?

"The safe limit of DER — the maximum DER — is 4:1 for corporate taxpayers. This means a company's total debt must not exceed 4 times its total equity," wrote KPP Pratama Maumere in an educational post on social media, as quoted on Thursday (28/5/2026).

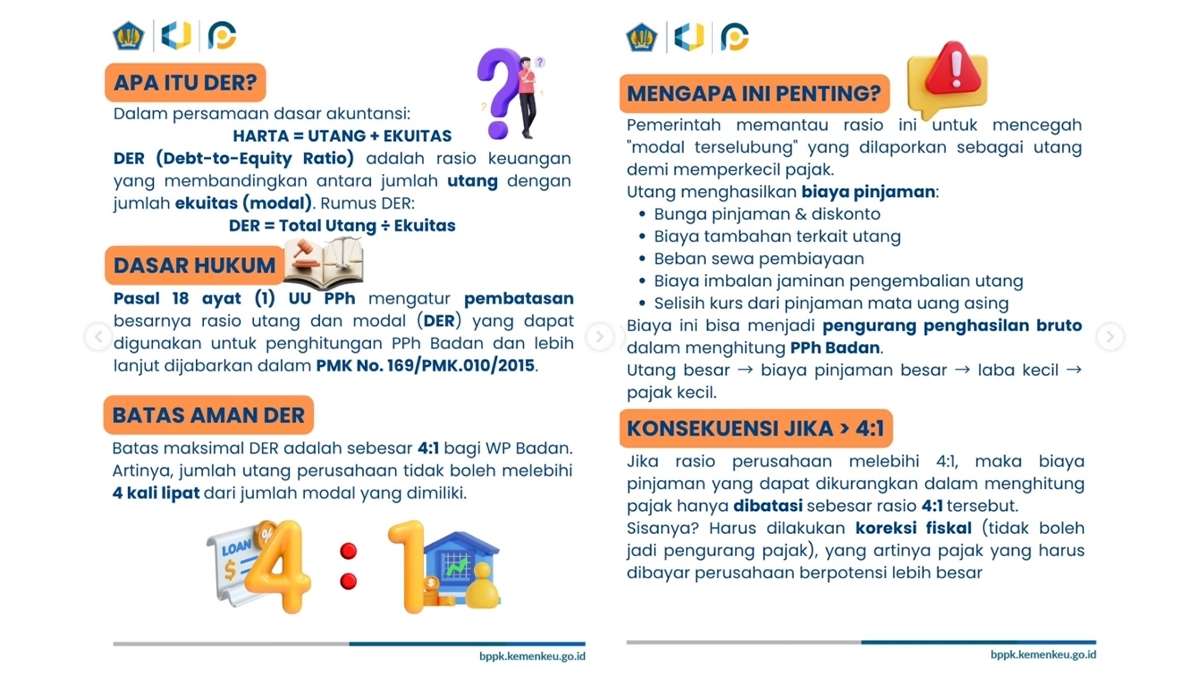

Before going further, taxpayers need to revisit what DER means. In accounting, the following formula is well known: Assets = Liabilities + Equity.

DER is a financial ratio that compares the total amount of debt to the total amount of equity (capital). The formula is: DER = Total Debt : Equity. The DER provisions are regulated under Article 18 paragraph (1) of the Income Tax Law. This provision regulates the limitation on the debt-to-equity ratio (DER) that may be used in the calculation of corporate income tax, and is further elaborated in PMK 169/2015.

DJP explains that the government monitors this ratio to prevent 'hidden capital' being reported as debt to reduce taxes. Debt generates borrowing costs, including loan interest and discount, additional costs related to debt, finance lease charges, debt repayment guarantee fees, and foreign exchange differences on foreign currency loans.

These costs can serve as deductions from gross income in the calculation of corporate income tax. This means that large debt leads to large borrowing costs, which reduces profits, and ultimately results in lower taxes.

If the debt ratio exceeds 4:1, the borrowing costs deductible in calculating tax are limited to the 4:1 ratio. The remainder must undergo a fiscal correction (cannot be used as a tax deduction). This means the tax a company must pay could potentially increase.

However, it should be noted that not all taxpayers are subject to this 4:1 rule. This provision does not apply to bank and financing institution taxpayers, insurance and reinsurance taxpayers, oil and gas and general mining taxpayers with contracts containing their own DER provisions, taxpayers engaged in infrastructure businesses, and taxpayers whose entire income is subject to final income tax.

In addition, the 4:1 DER provision only applies to corporate taxpayers, entities established or domiciled in Indonesia whose capital is divided into shares. This means CVs, partnerships (firma), cooperatives, foundations, and similar entities are not required to comply with the 4:1 DER rule.

"This DER rule does not mean companies are prohibited from taking on debt. However, if a company's debt is too large, the borrowing costs that may be charged for tax calculation purposes must be limited. What is being regulated is the tax effect of debt," wrote KPP Pratama Maumere.

Additionally, all borrowing costs — if the equity balance is zero or negative — and borrowing costs for private foreign debt, if such private foreign debt is not reported to DJP, cannot be taken into account in the calculation of taxable income.

DJP reminds taxpayers to use the average balance at the end of each month within one tax year or part of a tax year. This is in accordance with PMK 169/2015. Debt balances include both short-term and long-term debt.

"What is examined is the comparison of debt and equity throughout the year, not just at year-end," wrote DJP.

Therefore, companies need to maintain a balance between debt and equity. Poor financial planning should not end up increasing a company's tax burden. (sap)